All electric cars, whether fully electric or hybrid, need some form of battery. By far the most dominant form of electric vehicle battery over the last few years is the lithium nickel manganese cobalt oxide, or NMC battery, but a new type of battery is on the rise. Lithium iron phosphate batteries, or LFPs, are quickly gaining market share. According to the IEA, in 2022 NMC batteries accounted for 60% of the global market share, while LFPs accounted for 30%. According to S&P Global, by 2030 NMC market share is expected to decline to 42% while LFP market share will grow to about 41%.

LFP batteries are significantly less expensive than NMC batteries, and the cost difference between the two, plus LFP performance enhancements, could help push electric vehicle adoption rates higher which in turn would fuel further growth in the lithium battery market.

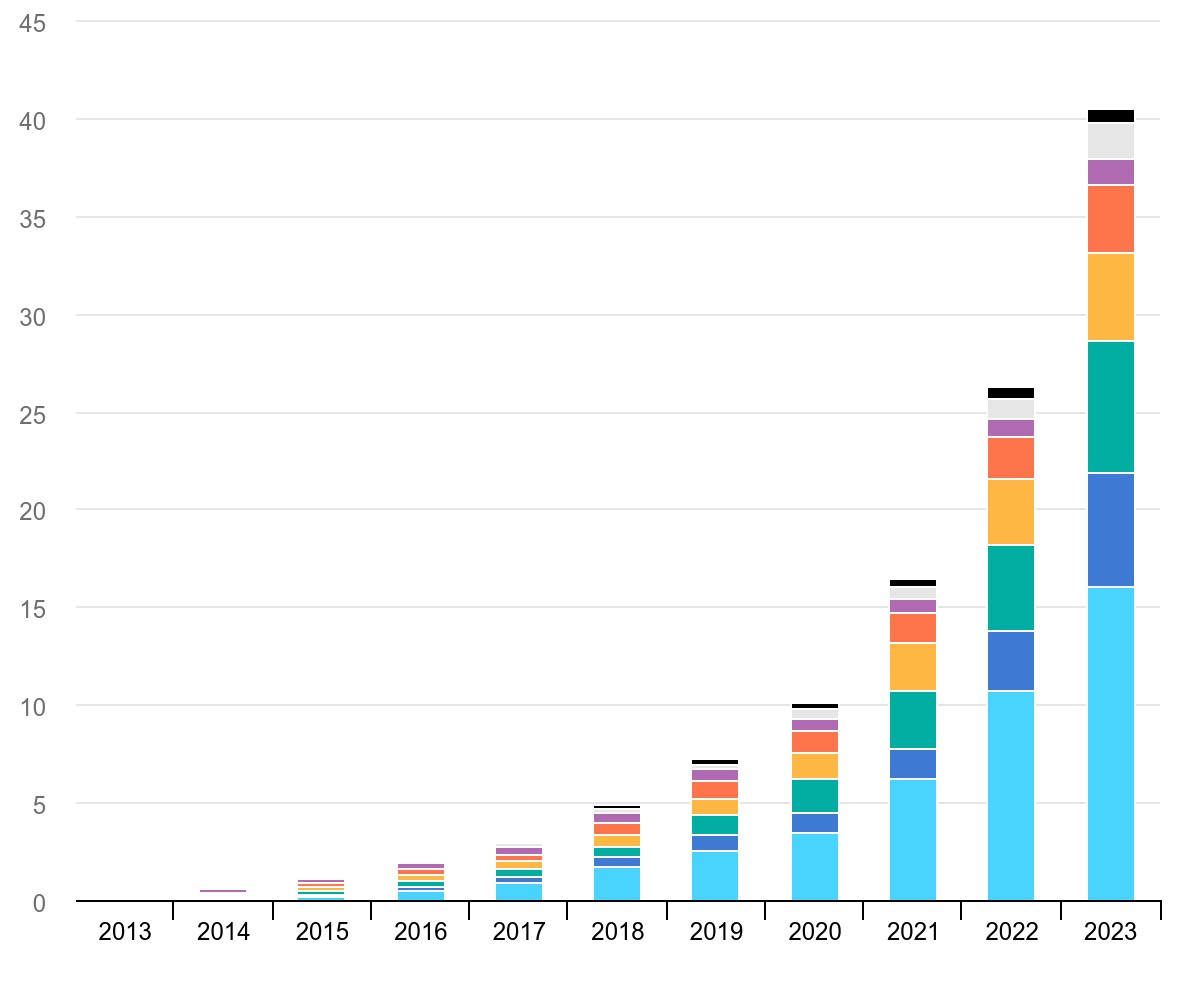

Electric vehicle sales, the main force behind the lithium battery revolution, have been rising considerably. According to the International Energy Agency (IEA), global electric car sales increased 35% from 2022 to 2023, and have increased 500% since 2018. About 18% of all cars sold were electric in 2023, up from 14% the year prior.

Global electric car stock, 2013-2023

These are impressive growth rates, and the trend is expected to continue. Already in the first quarter of 2024, sales grew about 25% compared to the same period in 2023. The first quarter 2024 sales numbers are about equal to the number of EVs sold in all of 2020. According to the IEA, substantial investment in the electric vehicle supply chain, ongoing policy support, and declines in the price of EVs and their batteries are expected to produce even more significant changes in the years to come. The Outlook finds that under today’s policy settings, every other car sold globally is set to be electric by 2035. Meanwhile, if countries’ announced energy and climate pledges are met in full and on time, two in three cars sold would be electric by 2035.

Why Are LFPs Rising?

LFP batteries are becoming more popular than NMC batteries for one main reason: lower price. The lower price is largely due to the materials used in the batteries. NMC batteries have a substantial amount of nickel and cobalt in them, generally expensive metals, with about 63% of raw material costs coming from lithium hydroxide. Meanwhile, lithium carbonate comprises about 89% of raw material costs in LFP batteries.

NMC batteries can usually charge more quickly, especially in cold weather, and have historically offered more range for drivers due to a higher energy density. However, they generally last two to three years, compared to perhaps ten years for LFPs. As with anything, there are pros and cons for each solution. However, recent advances in LFP battery technology have closed the gap for charging times, and long charging times are another main deterrent to EV adoption.

General Motors recently announced it will be switching from NMC to the most advanced LFP batteries on the market in its next generation of EVs, set to debut in 2025. The batteries, as with almost all EV batteries, are made in China. In this case, battery giant CATL has designed an LFP battery that can fully charge in ten minutes under ideal conditions. In just five minutes it can add about 125 miles of range. Importantly, GM estimates that it can shave $6,000 off the cost of producing its new EVs, due in large part to the switch to LFP batteries.

How to Invest

With the vast majority of the battery production located in China, that avenue is not available to western investors. Companies like GM and other major automakers are certainly an avenue to explore but are not necessarily pure plays in the EV market. Tesla is a pure play, and it’s likely that anyone interested in investing in the EV boom has already visited that opportunity.

The common thread through the whole industry, regardless of battery chemistry, is lithium. While the price of various forms of lithium has dropped significantly from recent historic highs, coming down 20% to 30% in 2024, the lower prices have in many ways allowed for LFP battery cost savings that could drive increased demand in the coming years. The price of LFP batteries in China has dropped 51% over the past year or so, to about $53 per kilowatt-hour compared to highs of $95 per kilowatt hour in 2023.

The drop in lithium prices completely changes the economics of lithium mining projects. Though analysts think the price is at its bottom this year, around $10,500/tonne, the effects throughout the industry have been widespread. The previous supply squeeze led to the meteoric rise of prices which in turn spurred more investment and higher production levels by current producers. In 2023 lithium output was 26.6% higher than in 2022, and 75.5% higher than in 2021.

“We are seeing a curtailment in nonessential capital expenditure from incumbent producers and an emphasis on operating cost improvement initiatives,” Chris Williams, lithium analyst at Adamas Intelligence, said in an email. Current market prices are hitting lower-grade spodumene concentrate and lepidolite producers the hardest because they often face higher production costs than brine and tier 1 producers, Williams said.

Note the focus on brine production as a cost-effective approach even at the reduced prices.

Lithium South’s HMN Li Brine Project

Lithium South Development Corporation (TSX-V: LIS) (OTCQB: LISMF) has been steadily advancing the Hombre Muerto North Lithium (HMN Li) project in Argentina’s Lithium Triangle. HMN Li features a measured and indicated lithium carbonate equivalent resource of 1,583,200 tonnes, with 90% of the resource falling in the measured category, the highest resource classification available. (Note 1)

Lithium South commissioned a Preliminary Economic Assessment (PEA) to outline the potential for developing a mine on the site that would start production in 2029. The estimate is eye-opening for a company currently valued in the $13 million range. Utilizing an annual production rate of 15,600 tonnes of lithium carbonate annually, the PEA maps out a mine life of 25 years with a 2.5 year payback period. After tax, the project has a Net Present Value of $934 million resulting in a 31.6% Internal Rate of Return. All of the anticipated capital costs and operating expenses are figured into the results, and a market lithium price of $20,000/tonne is used in the calculation. (Note 2)

An earlier PEA for the project, from 2019, used a price assumption of $12,420/tonne and an annual production rate of 5,000 tonnes annually. Advances in mining techniques along with an expansion of the resource estimate account for the difference in production rate between the two estimates. The after-tax Net Present Value came in at $217 million with an Internal Rate of Return estimated at 28%. (Note 3)

Either way you slice it, HMN Li looks like an intriguing project in today’s market and offers clear upside potential for investors. The exit strategy likely consists of either an acquisition by a battery maker or EV producer looking to secure supply for the long term, or possibly an offtake agreement with a similar company that isn’t willing or able to buy the whole project.

Interestingly, Lithium South has been able to produce, on a laboratory scale, lithium iron phosphate directly from its concentrated brine from the HMN Li project. The material was then used by an Argentine government agency to make an operating LFP battery. It’s a major step for the company as it seeks to develop capacity for higher-priced lithium products.

Lithium South is in the midst of completing an Environmental Baseline Study that will inform an Environmental Impact Report, essential for the company to receive the necessary permits for construction. There is also a Feasibility Study in the works that will update the whole project and set the table for actual mine development.

The Upshot

With LFP batteries fueling growth in the EV market, the demand for lithium is only going to increase. Current economics point to projects like HMN Li as brine sources are more affordable than hard rock mining sources. Investors looking for significant upside should probably be looking at emerging brine projects with proven resources and a path to production in the next few years. There is still value to be found in the EV battery industry, you just have to know where to look amid the changing market dynamics.

Note 1: September 12, 2023 / National Instrument 43-101 resource calculated by Groundwater Insight Inc. (GWI) of Halifax, Nova Scotia, Canada, report SEDAR filed November 6, 2023 / Updated Mineral Resource Estimate – Hombre Muerto North Project, NI 43-101 Technical Report Catamarca and Salta, Argentina, Mark King, PhD, PGeo, Peter Ehren, M.Sc, MAusIMM, September 5th, 2023.

Note 2: News release March 1, 2024 The PEA was prepared by Knight Piésold Consulting (“KP”) and JDS Energy and Mining (“JDS”), both of Vancouver, in accordance with the standards set out in National Instrument 43-101 Standards of disclosure for Mineral Projects (“NI 43-101”), and CIM’s Best Practice Guidelines for Mineral Processing (“BPGMP”).

Note 3: News release August 12, 2019 The PEA was prepared by Knight Piésold Consulting (“KP”) and JDS Energy and Mining (“JDS”), both of Vancouver, in accordance with the standards set out in National Instrument 43-101 Standards of disclosure for Mineral Projects (“NI 43-101”), and CIM’s Best Practice Guidelines for Mineral Processing (“BPGMP”).

Disclaimer: TDM Financial is paid a fee of $ U.S. 10,000 per month by Lithium South Development Corp (LIS) for advertising consultation. TDM Financial produced this advertisement on behalf of LIS and as such it should be considered advertising. Nothing written in this advertisement is meant to facilitate a trade in the shares of LIS, and is not to be considered investment advice. This advertisement is published for information purposes only and the reader is encouraged to do his/her own due diligence regarding LIS.

This advertisement contains certain “forward-looking statements” within the meaning of Section 21E of the United States Securities and Exchange Act of 1934, as amended. Except for statements of historical fact relating to the Company, certain information contained herein constitutes forward-looking statements. Forward-looking statements are based upon opinions and estimates of management at the date the statements are made and are subject to a variety of risks and uncertainties and other factors which could cause actual results to differ materially from those projected in the forward-looking statements. The reader is cautioned not to place undue reliance on forward- looking statements. We seek safe harbor.

Mr. William Feyerabend, a Consulting Geologist and Qualified Person under National Instrument 43-101, participated in the production of this advertisement and approves of the technical and scientific disclosure contained herein.