Saturn Oil & Gas Inc. (TSX-V: SOIL) quietly announced a transformational acquisition in May 2021. After starting negotiations when oil prices were near their pandemic-driven lows in 2020, the company finalized a leveraged buyout of a huge light oil producing asset in June 2021, making it one of the leading oil & gas producers and landholders in Southeast Saskatchewan.

Let’s look at the unique acquisition and why investors may want to pay closer attention to the stock.

A Remarkable Acquisition

Saturn Oil & Gas acquired over 450 net sections of land and 6,400 boe/d of production from Crescent Point Energy Corp. in the Oxbow area of Southeast Saskatchewan for cash consideration of approximately $82 million. The company financed the deal, and required working capital, with an $87 million senior secured term loan and $32 million in private placements, creating significant leverage for existing shareholders to extract value.

It was the story of the minnow swallowing the whale in that the transaction increased Saturn’s production at the time by over 2,000%.

The timing could not have been better. Saturn started the negotiations in 2020 when oil prices were decimated. Oil prices had somewhat recovered by May 2021 when the deal was finalized with WTI averaging USD $65 per barrel. With oil prices now over $100, the acquired Oxbow asset has become a cash generating machine. Saturn forecasts the Oxbow asset will produce over $170 million of cash flow from operations in 2022, on an asset acquired for less than half that amount the year prior.

As part of the acquisition, the company did hedge a good portion of the production. The company calculates about 66% of 2022 expected oil and liquids production will be hedged at prices closer to those of May 2021. However, over time Saturn expects to grow out of its declining hedges with 55% of production hedged for 2023, based on research analysts consensus of growth. The key value driver is incremental oil volumes from growth capital are fully-exposed to commodity prices and the hedges are reduced yearly. As a result, the company has an launched ambitious capital spending program for 2022 totalling $56 million for the drilling of 40 horizontal wells. It is the largest budget in the company’s short history and quite significant relative to its current $95 million market capitalization.

But, despite its hedged production, the company expects to generate enough free cash flow to repay its senior term loan, have zero net debt within 18 months and still fund a growth focused drilling program.

The company released financial and operational guidance on May 16, 2022 and forecasts 2022 cash flow per share (Adjusted funds flow) between $2.41 and $2.55 per basic share. With Saturn’s shares recently trading below $3.00 and therefore under 1.5 times cash flow it is relatively inexpensive versus its Canadian oil weighted peers on this metric. And since it’s a mature asset, the project has a very low decline rate (13%) and a 19-year reserve life, translating to robust free cash flow over the coming years for shareholders.

Liabilities Become Assets

Saturn Oil & Gas inherited an approximately $70 million clean-up liability with the asset based on inactive wells, which concerned many investors at first glance. However, the sharp rise in oil prices has made it more economical to repair these inactive wells and bring them back into production. In other words, the company has the potential to convert a liability into a cash-flowing asset.

The Oxford property has about 1,600 non-producing wells, and the company anticipates optimizing and recompleting more than 400 of them with low capital expenses over the next few years. With about $4 million of annual workover cap-ex, the company believes it can offset much of the anticipated production declines at very economical rates of return while cleaning up the acquired asset.

In addition, the company plans to accelerate liability clean-up with the support of more than $13 million in federal Accelerated Site Closure Program funding and has posted a cash deposit of $21 million for future abandonment and reclamation obligations. The next 5+ years of asset clean up is prefunded. By eliminating the overhang, the company will have a fresh slate in the eyes of investors while improving its overall ESG performance for environmentally-conscious partners.

Q1 2022 Was Saturn’s Signature Quarter

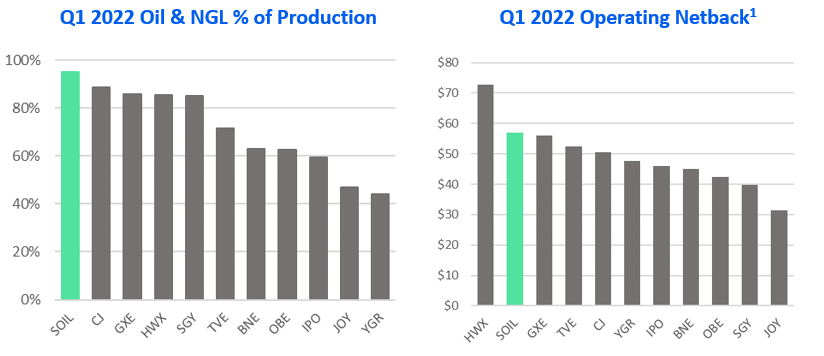

Saturn Oil & Gas has been trading for less than a year post the Oxbow acquisition so it is understandable many investors are hearing about this new oil company for the first time. However, its recent quarterly performance could change things. During the first quarter of 2022, the company reported $69 million in revenue, $16.3 million in EBITDA, $13.5 million in adjusted funds flow ($0.50 per basic share), on a 3,118% increase in production year over year. Q1 2022 was its fourth consecutive quarter posting record production levels and a solid start to posting a full calendar year of results with the Oxbow asset. The quarter results were testament to Saturn now having one of the highest oil production weightings of the conventional peer group which drives one the highest operating netbacks at $56.94 per.

Source: Saturn Investor Presentation and industry reports

Analysts See a Big Opportunity

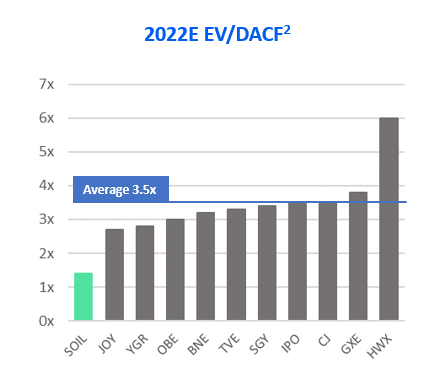

In recent weeks, two new investment dealers have launched research coverage of Saturn Oil & Gas to join Beacon Securities analyst Kirk Wilson, CFA, who was first in Canada with coverage on the company. Mr. Wilson recently issued a Buy rating and an $8.50 per share price target, reflecting a 200%+ premium to the current market price. After a strong quarter showing rising production and declining debt, the analysts believe investors will start to notice and help it obtain a more realistic EV/DACF (EBITDA) multiple. Currently Saturn Oil & Gas has the lowest multiple in the peer group on this metric:

Source: Beacon Securities Limited, May 4, 2022

Looking Ahead

Saturn Oil & Gas Inc.’s (TSX-V: SOIL) savvy acquisition last year has now laid the framework for years of organic growth. The company has a portfolio of 351 booked drilling locations with reserves and hundreds more of unbooked locations to supply over a decade’s worth of drilling. And with the current high oil prices, Saturn Oil & Gas has the internal generated cash flow to fund its growth drilling plans while it rapidly pays off its acquisition debt. With hedges in place protecting the downside and plans to rework hundreds of wells, the company’s in a great position to unlock long-term shareholder value.

In the meantime, the stock trades at a fraction of its peers’ valuation, providing a unique opportunity for investors. For more information, visit the company’s website or download their investor presentation.

Disclaimer

The above article is sponsored content. CFN Media, has been hired to create awareness.